Unlocking Tax Savings: Your Comprehensive Guide to Reducing your Tax Bill

As the Income Tax Return deadline approaches this October, many individuals find themselves facing the prospect of taxes owed to Revenue. But fear not! In this informative blog series, we delve into a variety of strategies and opportunities to empower you in minimising your tax obligations.

One avenue to consider is harnessing the power of pensions. Pensions represent a tax-efficient method of saving, with the government extending enticing tax incentives tailored to your highest income tax bracket. These incentives encourage individuals to actively contribute to their pension plans, securing their financial future.

Pension contributions to the following pension plans may qualify for tax relief:

- occupational pension schemes

- Personal Retirement Savings Accounts (PRSAs)

- Retirement Annuity Contracts (RACs)

- Pan-European Personal Pension Products (PEPPs)

- qualifying overseas plans.

The extent of tax relief available hinges on factors such as your age and annual earnings, which dictate the maximum allowable pension contribution eligible for these tax benefits. Tax relief for employee pension contributions is subject to two main limits:

- an age-related earnings percentage limit

- a total earnings limit.

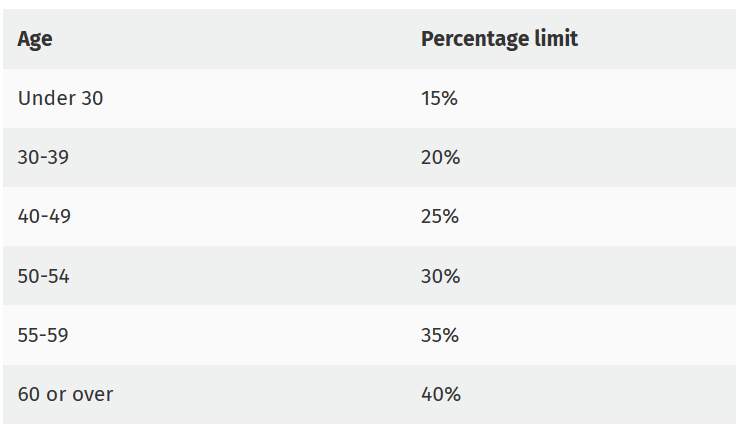

Age-Related Earnings Percentage Limit

You can get tax relief up to the relevant age-related percentage limit of your earnings in any year. Relief is only available from the source of income in respect of which the contributions are made.

For example, John is aged 48 and earns €40,000 per year. John can claim tax relief on pension contributions up to €10,000 per year.

Total Earnings Limit

The maximum amount of earnings that can be taken into account for tax relief is €115,000 per year.

But that’s not all! By taking action and making a pension contribution before the impending October 31, 2023 deadline, you can choose to apply this relief to reduce your tax obligations for the year 2022.